Retirement Planning Basics: When and How Much to Save

Learn when to start saving for retirement and how much you really need to put away each year. Discover proven strategies to build a secure retirement even if you're starting late.

View MoreWhen you think about retirement savings, money set aside to support your lifestyle after you stop working. Also known as retirement nest egg, it’s not just about how much you save—it’s what you save it in, and how you keep it safe as you age. Too many people assume that if they max out their 401(k), they’re done. But that’s like buying a car and never checking the tires. Your savings need to work for you, not just sit there.

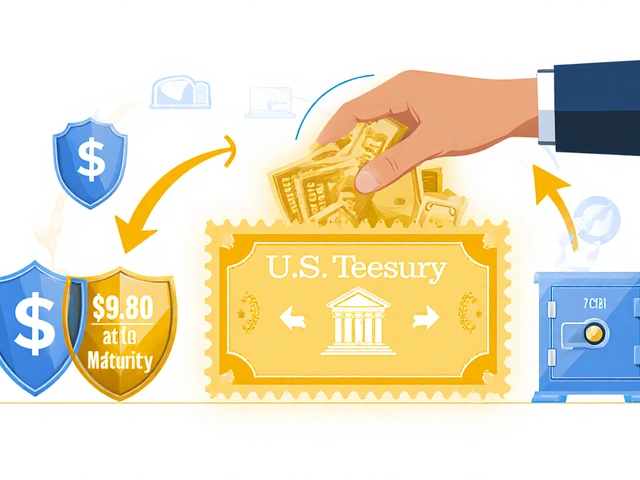

Treasury bills, short-term government securities that pay interest with almost zero risk are the quiet backbone of smart retirement planning. If you’ve got an emergency fund, you’re probably already using them—because they’re safer than your savings account and pay more than 5% right now. And when you’re close to retirement, that safety matters more than chasing high returns. Dividend stocks, companies that pay you a share of profits regularly can give you cash flow without forcing you to sell shares. That’s huge when the market dips and you need income, not a paper loss. These aren’t just investment options—they’re tools that help you turn savings into reliable income.

Then there’s Social Security, a government program that pays monthly income based on your work history. It’s not going to cover everything, but it’s the foundation most people rely on. When you claim it—early, at full retirement age, or delayed—changes how much you get every month for the rest of your life. And if you pair it with dividend-paying stocks that grow over time, you can reduce how much you need to pull from your savings each year. That’s the real secret: it’s not about how much you saved, it’s about how you stretch it.

You won’t find a single magic formula for retirement savings. But you will find patterns in what works: people who avoid big losses, who use income streams instead of just selling assets, and who understand the timing of Social Security. The posts below cover exactly that—how to spot a dividend trap before it ruins your income, how T-bills beat high-yield savings accounts for safety, how to coordinate your Social Security claim with your other accounts, and why your emergency fund shouldn’t be stuck in a checking account. These aren’t theory pieces. They’re real tools used by people who retired without running out of money.

Learn when to start saving for retirement and how much you really need to put away each year. Discover proven strategies to build a secure retirement even if you're starting late.

View More