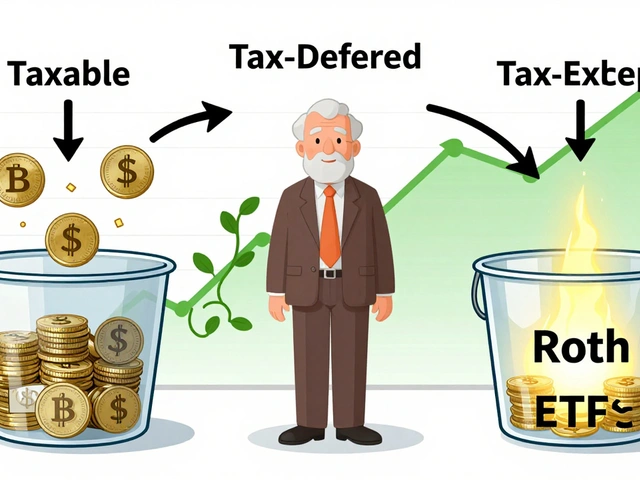

Taxable Brokerage Account: What It Is and When to Use One

When you open a taxable brokerage account, an investment account where you buy and sell stocks, bonds, or funds without tax advantages. Also known as a non-retirement investment account, it gives you total freedom to deposit, withdraw, or trade whenever you want—but you owe taxes on every dividend and profit. Unlike a Roth IRA or 401(k), there are no income limits, no contribution caps, and no penalties for early withdrawals. That flexibility comes at a cost: you pay capital gains tax, the tax you pay when you sell an investment for more than you paid for it on short-term gains (held less than a year) and lower long-term rates if you hold longer. You also pay tax each year on dividends, payments companies make to shareholders, whether you reinvest them or not.

So why would anyone choose this over a tax-free retirement account? Because retirement accounts have limits. If you’ve maxed out your 401(k) and Roth IRA and still want to save more for a house, a business, or early retirement, a taxable brokerage account is your next tool. It’s also the only way to invest for goals that don’t fit the timeline of retirement—like paying for a wedding in five years or funding a child’s college education. Many people use it as a bridge between retirement savings and short-term goals. And when you’re rebalancing your portfolio, you can be smarter about it: sell losing positions in your taxable account to offset gains, while holding winners in your Roth IRA to avoid taxes entirely. That’s tax-aware rebalancing, a strategy that moves assets between taxable and tax-advantaged accounts to reduce your overall tax burden—something you can’t do if you only use retirement accounts.

There’s no one-size-fits-all answer. If you’re young and just starting out, focus on maxing out your 401(k) and Roth IRA first. But if you’re saving for something specific that’s not retirement, or you’ve already hit your retirement limits, a taxable brokerage account isn’t just an option—it’s your best next move. Below, you’ll find real breakdowns of how to use it, when to avoid it, and how to minimize taxes without giving up growth. No jargon. No fluff. Just what works.