Emergency Fund Setup Checker

Emergency Fund Setup Assessment

Answer these quick questions to determine which emergency fund approach works best for you. Based on your answers, we'll recommend the most effective setup for your situation.

Your Personalized Emergency Fund Recommendation

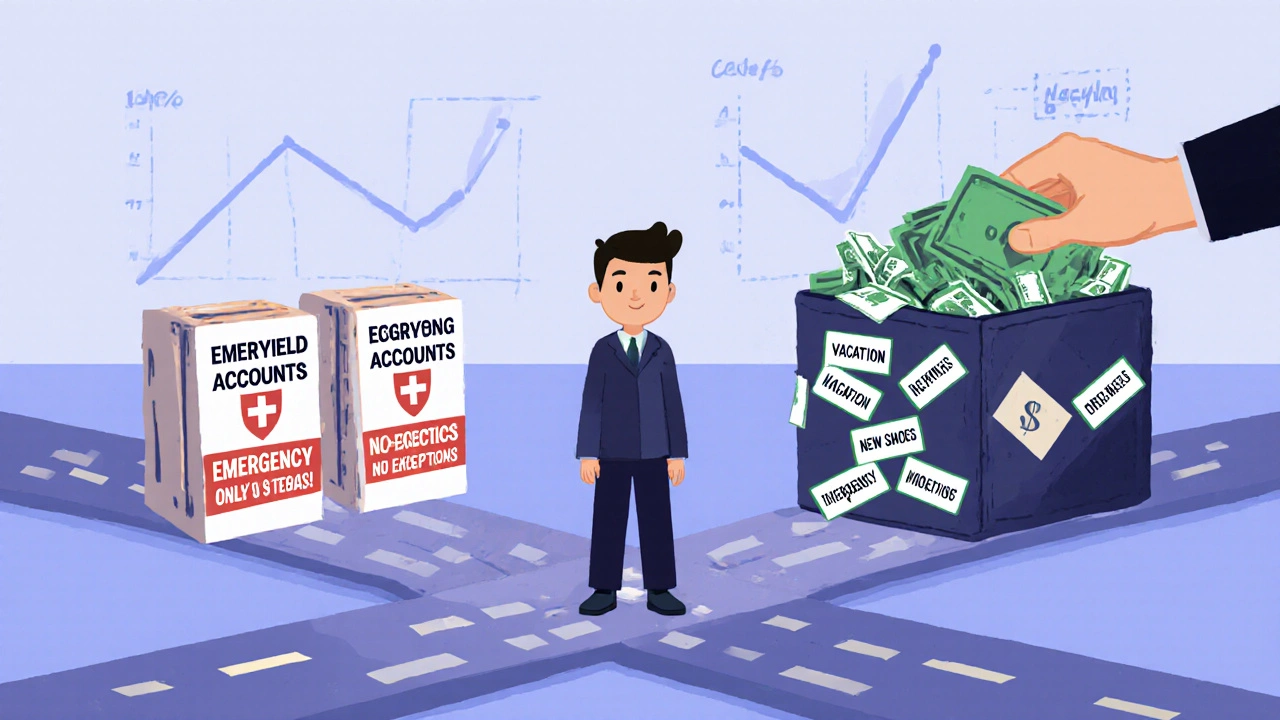

Separate Account Approach Recommended

Based on your answers, keeping your emergency fund in a separate account is the best choice for you. This creates a psychological barrier between your emergency savings and other funds, reducing the temptation to dip into it for non-essential expenses.

- 82% of financial planners recommend this approach for beginners and those with less discipline

- 73% of beginners who use separate accounts reach their emergency fund goal

- Prevents accidental use for non-emergencies like vacations or shopping

Why this works for you: Your answers indicate you may have a tendency to use savings for non-emergencies and may not track your spending closely. A separate account provides the necessary separation to protect your emergency fund.

How to Implement This Approach

- Open a high-yield savings account (Ally, Marcus, or Discover)

- Label it clearly: "Emergency Fund Only. No Exceptions."

- Set up an automatic transfer of $50-$200 per paycheck

- Leave it alone except for true emergencies (job loss, medical bills, major repairs)

Your Personalized Emergency Fund Recommendation

Combined Account Approach Recommended

Based on your answers, using a single account with clear tracking is the best approach for you. This works well if you're disciplined with budgeting and have a strong history of meeting savings goals.

- Works best for those who track every dollar spent

- Can be effective if you've never raided your savings for non-emergencies

- Less account management

Why this works for you: Your answers show you're disciplined with tracking your spending and have a history of meeting savings goals. This allows you to manage multiple goals within one account.

How to Implement This Approach

Use a single high-yield savings account but track your emergency fund separately using:

- A spreadsheet or budgeting app like YNAB or Mint

- Sub-accounts within your savings account (Ally, Capital One, or Chime)

- Manual transfers between categories

Set clear rules for what counts as an emergency to avoid accidental depletion.

Your Personalized Emergency Fund Recommendation

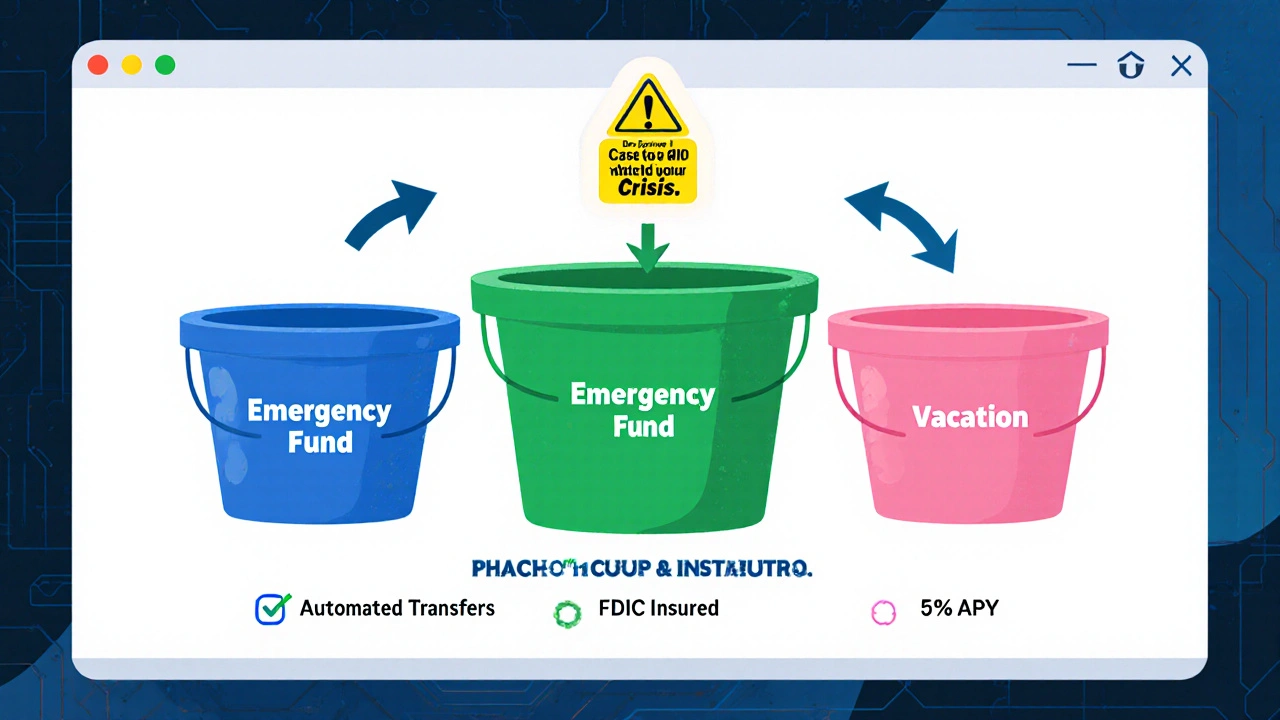

Hybrid Approach Recommended

Based on your answers, a hybrid approach that combines elements of both systems is ideal for you. This gives you the structure you need without overwhelming account management.

- One login and one interest rate

- Clear visual separation between goals

- Automatic transfers to each bucket

Why this works for you: Your answers indicate you're somewhat disciplined with spending but could benefit from additional structure. This approach offers the best of both worlds.

How to Implement This Approach

Use a bank that offers "buckets" or sub-accounts like Ally Bank, Capital One, or Chime. Create labeled categories:

- Emergency Fund (at least 3 months of expenses)

- Car Repair Fund

- Medical Expenses Fund

Set up automatic transfers to each bucket and manually move money only when necessary.

Why Your Emergency Fund Setup Matters More Than You Think

You’ve heard it a hundred times: build an emergency fund. But here’s the thing most people miss - it’s not just about how much you save. It’s about how you organize it. If your emergency money sits in the same account as your vacation fund or your new laptop savings, you’re setting yourself up for trouble. A 2023 study from the Journal of Consumer Research found that 68% of people who kept their emergency savings mixed with other goals ended up dipping into it for non-emergencies - like a weekend trip or a new pair of shoes. That’s not saving. That’s borrowing from your future self.

The Federal Reserve’s 2022 report showed that nearly 4 in 10 Americans couldn’t cover a $400 emergency without borrowing. That’s not because they’re bad with money. It’s because they never set up a system that actually works for their behavior. The right setup - whether separate or combined - can turn a $500 starter fund into a $10,000 safety net. The wrong one? It becomes a ghost account you forget about until you’re desperate.

What Exactly Is an Emergency Fund (And What It’s Not)

An emergency fund isn’t just any savings account. It’s a specific tool for unexpected, urgent, and unavoidable expenses. Think: a broken water heater at 2 a.m., a sudden medical bill, or losing your job. It’s not for planned expenses like a vacation, a new TV, or holiday gifts. Those are sinking funds - money you save over time for known future costs.

Experts like Suze Orman and Dave Ramsey have spent decades pushing the 3-6 month rule: save enough to cover your essential living expenses for that time frame. That means rent or mortgage, utilities, groceries, insurance, and basic transportation - not Netflix subscriptions or gym memberships. The goal isn’t luxury. It’s survival.

And here’s the kicker: your emergency fund should be in a high-yield savings account. As of Q3 2024, top options like Ally Bank (4.20% APY), Marcus by Goldman Sachs (5.00% APY), and Discover (4.30% APY) offer returns far better than traditional banks. These accounts are FDIC-insured up to $250,000, so your money is safe. And they let you access it in 1-3 business days - fast enough for real emergencies, slow enough to stop impulse spending.

The Separate Accounts Approach: Why Most Experts Recommend It

Eighty-two percent of certified financial planners surveyed by the Financial Planning Association in 2023 recommend keeping your emergency fund in a completely separate account from everything else. Why? Psychology.

When your emergency money lives in its own account, your brain treats it differently. You don’t see it as "extra cash." You see it as a lifeline. That mental separation makes it harder to spend. A Reddit user named u/SavingsWarrior put it bluntly: "I kept them combined for years and kept raiding it for vacations - separated them last year and now have $8,000 in emergencies versus $200 previously."

This approach works best for beginners, people who struggle with self-control, or anyone who’s ever said, "I’ll just take $500 from savings for this." The National Foundation for Credit Counseling found that 73% of beginners who used separate accounts actually reached their emergency fund goal - compared to just 39% who didn’t.

Setting it up is simple:

- Open a new high-yield savings account (Ally, Marcus, or Capital One are easy options).

- Label it clearly: "Emergency Fund Only. No Exceptions."

- Set up an automatic transfer of $50-$200 per paycheck.

- Leave it alone. Seriously. Don’t even check the balance unless something bad happens.

The downside? More accounts to manage. If you’re already juggling three checking accounts, three credit cards, and three investment accounts, adding another can feel overwhelming. That’s where the combined approach comes in.

The Combined Approach: When One Account Works Better

Some people - especially those with strong budgeting habits - do just fine with one account. They call it "naming your dollars." Instead of separate accounts, they use one high-yield savings account and track different goals with a spreadsheet or budgeting app like YNAB or Mint.

On the Mr. Money Mustache forum, user "BudgetWizard" shared: "We’ve used one account since 2016 with spreadsheet tracking - $28,000 total, $18,000 allocated to emergencies, zero overdrafts." That’s not luck. That’s discipline.

This method works best if:

- You’re already tracking every dollar you spend

- You have a history of sticking to budgets

- You’re comfortable with digital tools

- You’ve never raided your savings for non-emergencies

But here’s the risk: a 2023 EBNEMO study of 5,000 account holders found that people using combined accounts were 27% more likely to accidentally drain their emergency money. Why? Because when everything’s in one place, it’s easy to think, "I’ve got $20,000 saved - I can afford to spend $3,000 on a car repair," when that $3,000 was supposed to be for a job loss.

The FIRE (Financial Independence, Retire Early) community leans heavily into this model. But they’re not average savers. They’re typically high-income, highly disciplined, and have multiple income streams. If you’re not in that group, you’re playing with fire.

Hybrid Options: The Middle Ground

If you like the idea of one bank account but want mental separation, many banks now offer sub-accounts or "buckets" within a single savings account. Ally Bank, Capital One, and Chime all let you create labeled savings pots - like "Emergency," "Car Fund," and "Vacation" - all under one main account.

This gives you the best of both worlds:

- One login, one interest rate

- Clear visual separation between goals

- Automatic transfers to each bucket

It’s not perfect - you still have to manually move money between buckets if you need to use your emergency fund - but it’s far better than a single, unmarked account. Six percent of people surveyed in 2023 used this method, and 89% of them reported feeling more in control than before.

For most people, this is the sweet spot: simple enough to maintain, structured enough to prevent mistakes.

How Much Should You Actually Save?

There’s no magic number. But here’s what works in real life:

- Phase 1: $500. Get this first. It covers small emergencies - a flat tire, a broken appliance. The Consumer Financial Protection Bureau says you can hit this in 30 days with just $17 per paycheck.

- Phase 2: 1 month of expenses. Once you’ve got $500, aim for enough to cover one month of rent, groceries, and bills. This is your "don’t panic" buffer.

- Phase 3: 3 months of expenses. This is the standard goal for most people. If you have a stable job and health insurance, this is enough.

- Phase 4: 6 months of expenses. Only needed if you’re self-employed, single-income, or work in a volatile industry. It’s overkill for most.

Don’t try to do all four at once. Start small. Build momentum. A 2024 Ally Bank study found that people who automated even $25 per paycheck saved 2.3 times more than those who transferred money manually.

What to Avoid at All Costs

Here are the three biggest mistakes people make:

- Using a checking account. Too easy to spend. Too tempting to let your balance drop to zero.

- Investing it in stocks or crypto. Emergency funds need to be liquid and stable. If the market crashes, you can’t sell shares to pay your electric bill.

- Ignoring inflation. Cash loses value over time. A $10,000 emergency fund today will buy less in 2027. That’s why you need a high-yield account - to at least keep pace with inflation.

Also avoid accounts with minimum balances over $100. Bankrate’s 2023 churn analysis found that 43% of people abandoned accounts that required them to keep $300 or more. If you’re just starting out, you need flexibility, not penalties.

What the Data Says About Who Succeeds

There’s a clear pattern in who builds real emergency savings:

- Households earning over $100,000: 58% have separate emergency funds

- Households earning under $40,000: Only 22% do

- People with over $20,000 saved: 86% use separate accounts

- People with under $5,000 saved: 79% use combined accounts

It’s not about income. It’s about behavior. People who succeed don’t wait until they’re "ready." They start with $500 and build from there. They don’t obsess over the perfect account. They just pick one and automate it.

The most successful users - whether they use separate or combined accounts - all have one thing in common: they treat their emergency fund like a non-negotiable bill. Just like rent. Just like your phone plan. You pay it. Every time. No exceptions.

Future Trends: What’s Coming Next

Emergency fund strategies are evolving. In 2024, SoFi started piloting AI tools that detect when your income might drop - like if you’re working fewer hours - and automatically move extra cash into your emergency fund. Fidelity now recommends a "tiered" approach: 1 month in cash, 2 months in money market funds, 3 months in short-term bonds. It’s not for everyone, but it’s a sign that the old "cash-only" rule is getting a rethink.

Financial advisors are also starting to accept that rigid separation isn’t always best. The Financial Planning Association’s June 2024 update says: "While separate accounts remain ideal for most clients, disciplined investors may achieve equivalent outcomes through rigorous tracking."

That’s the future: more flexibility, more personalization. But for now, if you’re not sure what to do - go separate. It’s the safest, most proven path.

Should I keep my emergency fund in a separate account?

Yes, for most people. A separate account prevents you from accidentally spending your emergency money on non-emergencies. Studies show 68% of people who combine their savings end up raiding their emergency fund. A dedicated account creates a psychological barrier that protects your safety net.

Can I use one savings account for both emergencies and other goals?

You can, but only if you’re highly disciplined. You’ll need to track every dollar with a spreadsheet or app and never touch the emergency portion unless it’s a true crisis. For most people, the mental effort and risk of mistakes make this approach too dangerous. Beginners should avoid it.

How much should I have in my emergency fund?

Start with $500. Then aim for one month of essential expenses, then three months. If you’re the only income earner in your household or work in a volatile job, aim for six months. That’s enough to cover rent, utilities, food, and basic transportation if you lose your job.

Where should I keep my emergency fund?

In a high-yield savings account with no fees and FDIC insurance. Look for accounts offering 4.00-5.25% APY, like Ally Bank, Marcus by Goldman Sachs, or Discover. Avoid checking accounts, CDs, or investments. Your emergency fund needs to be safe, accessible, and earning interest.

Is it okay to use my emergency fund for a car repair?

Yes - if it’s unexpected and necessary. A sudden transmission failure or a broken-down vehicle that keeps you from work counts. But if you’ve been planning to replace your car for months, that’s a sinking fund, not an emergency. Don’t use your emergency fund for planned expenses.

What if I can’t save $500 right now?

Start with $25. Even $5 a week adds up. Automate it. Set up a transfer from your paycheck to a separate savings account, even if it’s just $10 per pay period. The goal isn’t perfection - it’s consistency. People who save $25 weekly reach $500 in under two months. That’s enough to handle most small emergencies.

Do I need more than one emergency fund?

No. One fund is enough. But if you want to organize it, use sub-accounts within your savings account (like Ally’s "buckets") to label portions as "Emergency," "Medical," or "Car." Don’t create separate accounts unless you’re confident you can manage them without confusion.

Next Steps: What to Do Today

Don’t wait for the perfect time. Here’s what to do right now:

- Open a high-yield savings account if you don’t have one. Ally or Marcus are easiest.

- Transfer $50 from your checking account. That’s your starter fund.

- Set up an automatic transfer of $25-$50 every payday.

- Label it clearly: "Emergency Fund Only. No Exceptions."

- Do not touch it unless you lose your job, have a medical emergency, or face a major home repair.

That’s it. You’ve just built a real safety net. In 12 months, you’ll have $1,200-$2,400. In two years? $2,400-$4,800. That’s not magic. That’s momentum. And momentum beats perfection every time.

Kenny McMiller

October 30, 2025 AT 01:43It's not about the account structure-it's about behavioral economics. The cognitive dissonance between mental accounting and actual spending behavior is the real bottleneck. When you treat money as fungible but your brain doesn't, you create a systemic leak. Separate accounts aren't about banking-they're about neuroeconomic friction. You're not saving money; you're engineering self-control through environmental design. The Fed data doesn't lie: 40% of Americans can't cover $400 because they're optimizing for immediate gratification, not long-term resilience. The account is just the container. The real work is in the wiring of your default behaviors.

Dave McPherson

October 30, 2025 AT 11:38Lmao. So you're telling me the only reason people can't save is because they're too lazy to open a second account? Bro. I've got a single account with 17 custom-named buckets in YNAB, a macro that auto-tags every transaction, and a spreadsheet that updates in real-time with my bank's API. I've saved $42k in 4 years. The real problem isn't your bank-it's your brain. If you need a separate account to not spend your emergency fund, you're not a saver-you're a toddler with a debit card. The FIRE crowd doesn't use separate accounts. They use discipline. And if you can't handle one account, maybe you shouldn't be allowed to touch money at all. 😴

RAHUL KUSHWAHA

October 31, 2025 AT 01:32