Separate Emergency Fund: Why It’s the First Rule of Smart Investing

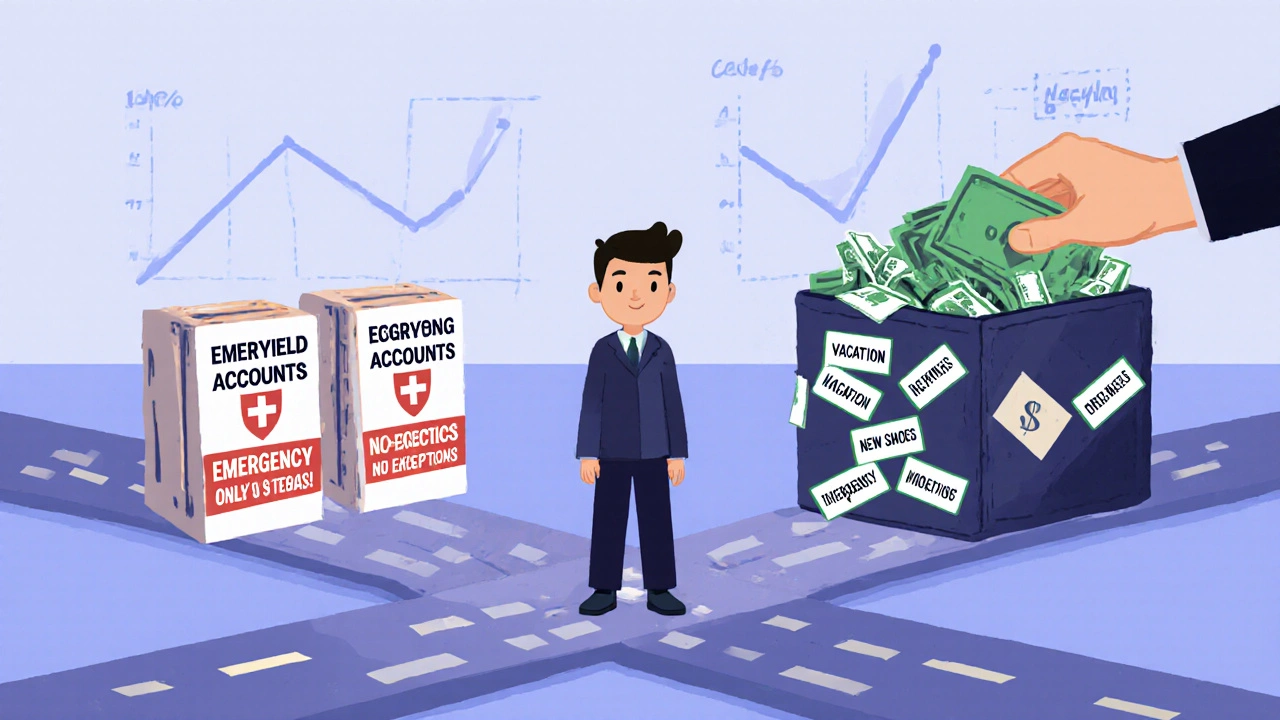

When you’re building wealth, the most important money you’ll ever manage isn’t in your brokerage account—it’s in your separate emergency fund, a dedicated cash reserve kept completely apart from your investments to cover unexpected costs without touching your portfolio. Also known as a financial safety net, this fund isn’t about earning returns—it’s about staying in the game when life throws a curveball. If you dip into your 401(k) or sell stocks during a market dip to pay a medical bill or fix your car, you’re not just losing cash—you’re losing time, compounding, and peace of mind.

A cash reserve, a liquid, easily accessible pool of money held in a high-yield savings account or similar low-risk vehicle should never be confused with your investment accounts. That’s the mistake most beginners make. They think a Roth IRA or taxable brokerage account can double as an emergency fund. But those are growth tools, not safety tools. Selling shares when you need cash means locking in losses, paying taxes, and missing future gains. A financial safety net, a buffer that keeps you from making panic-driven financial decisions works because it’s out of reach—literally and psychologically. You don’t touch it unless you absolutely have to.

How much should you keep? Three to six months of living expenses is the standard, but it’s not magic—it’s practical. If you work freelance, have kids, or live in a high-cost area, lean toward six. If you’re on a stable salary with good benefits, three might be enough. The key isn’t the number—it’s the separation. Keep it in a different bank, with different login credentials, so you don’t accidentally spend it. Treat it like your retirement account: invisible, untouchable, and sacred.

And here’s the truth most guides won’t tell you: your separate emergency fund isn’t just protection—it’s permission. Permission to invest boldly. Permission to hold through market crashes. Permission to say no to bad jobs or toxic situations because you’re not one unexpected bill away from disaster. Every post in this collection—from tax-aware rebalancing to robo-advisor support—assumes you’ve got this base covered. Without it, even the smartest investment strategy falls apart.

Below, you’ll find real, practical guides that build on this foundation. Learn how to structure your accounts so your emergency fund stays safe while your investments grow. See how automation and tax strategies work better when you’re not scrambling for cash. And understand why financial tools like taxable brokerage accounts and retirement plans only make sense when you’ve got this first layer locked down.