High-Yield Savings Account: What It Is and How to Use It Right

When you put money in a high-yield savings account, a type of savings account that pays significantly higher interest than traditional banks. Also known as online savings account, it’s one of the safest ways to grow your cash without touching the stock market. Unlike regular savings accounts that might pay 0.01% interest, a good high-yield account pays 4% to 5% right now—meaning $10,000 earns you $400 to $500 a year, tax-deferred, with zero risk.

This isn’t magic. It works because online banks don’t have branches, so they save money and pass it to you in the form of better rates. And yes, it’s still FDIC insured, federal protection that covers up to $250,000 per person, per bank. That means even if the bank fails, your money is safe. You don’t need to be rich to use one. You don’t need to be an expert. You just need to know where to look. Many people still use big-name banks because they’re familiar—but they’re leaving hundreds of dollars a year on the table.

Think of a high-yield savings account as your financial parking spot. It’s not for long-term growth like stocks or real estate. It’s for money you need soon—emergency funds, vacation savings, a down payment, or cash you’re saving for a big purchase. Keeping that money in a regular account is like letting it sit in a drawer with no interest. With a high-yield account, it’s working for you while you wait.

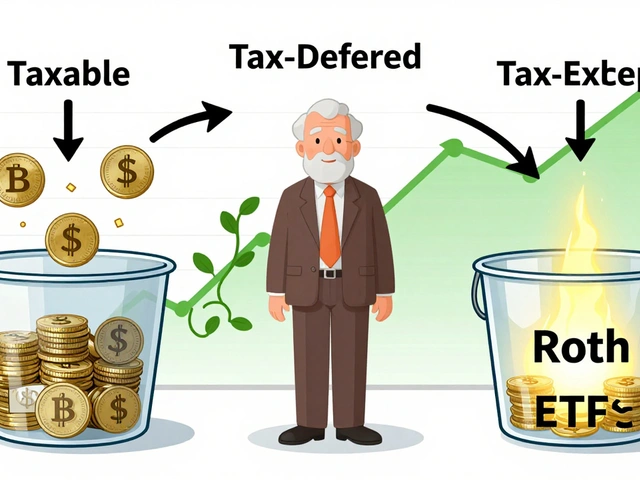

It also plays well with other tools. If you’re using a taxable brokerage account, a flexible investment account where you pay taxes on gains and dividends. you can move money between them strategically. Keep your short-term goals in the high-yield account. Let your long-term goals grow in the brokerage. That’s tax coordination in action—simple, smart, and proven to add up over time.

Some people confuse it with certificates of deposit (CDs) or money market accounts. CDs lock your money for months or years. Money market accounts might offer higher rates but often come with minimum balances and transaction limits. A high-yield savings account gives you flexibility: withdraw when you need to, no penalties, no strings attached. And unlike stocks, there’s no market crash to worry about. Your balance doesn’t drop because the economy stumbles.

Right now, interest rates are high. That won’t last forever. When the Fed cuts rates, these accounts will drop too. But even then, they’ll likely still outpace traditional banks. The best time to open one was years ago. The second best time is today.

You’ll find posts here that explain how to compare rates, avoid hidden fees, and use these accounts alongside other financial tools. Some show you how to layer them with earned wage access programs to smooth cash flow. Others break down how they fit into broader strategies like tax-aware rebalancing or building multiple account types. This isn’t about getting rich overnight. It’s about making your money work harder—without taking unnecessary risks.