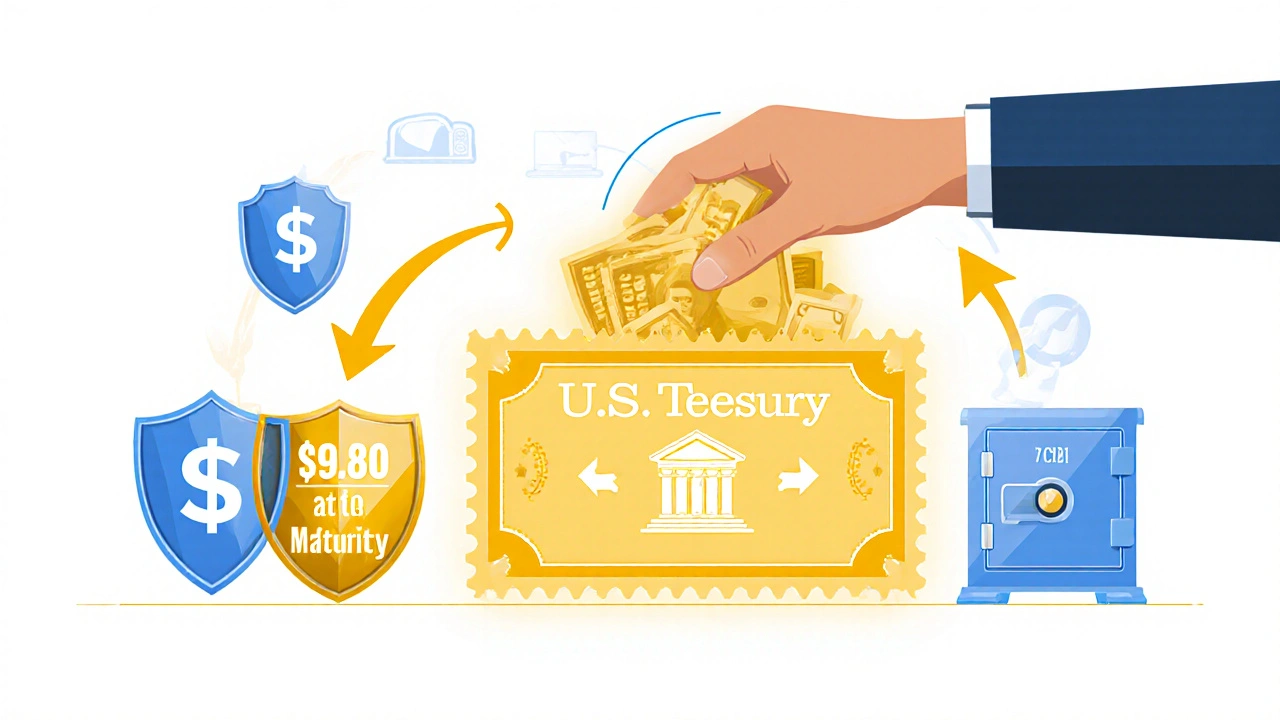

Government Securities: Safe Investments Backed by the U.S. Treasury

When you buy a government security, a debt obligation issued by the U.S. Treasury to fund federal spending. Also known as Treasuries, these are among the safest investments in the world because the U.S. government backs them with its full faith and credit. If you’re looking for stability—especially when markets get wild—government securities are one of the few places your money can sit without fear of default.

There are three main types: Treasury bills, short-term securities maturing in up to one year, Treasury notes, medium-term bonds paying interest every six months and maturing in 2 to 10 years, and Treasury bonds, long-term investments that last 20 or 30 years. You can buy them directly from TreasuryDirect.gov, through a broker, or even in mutual funds. They’re not flashy, but they’re the bedrock of many portfolios.

Why do investors turn to them? Because they reduce risk. When stocks drop, Treasuries often rise. They’re the counterbalance to volatile assets like growth stocks or options. Even if you’re not chasing high returns, you still need these to protect your capital. And unlike corporate bonds, there’s almost no chance of losing your principal—if you hold to maturity.

They also play a role in retirement planning. Many people use Treasury securities to generate steady interest income without touching their principal. That’s why they show up in discussions about dividend safety, emergency funds, and asset allocation. You don’t need to be a Wall Street pro to use them—just someone who wants to avoid unnecessary risk.

What’s interesting is how they interact with interest rates. When the Fed raises rates, new Treasuries pay more—but existing ones drop in price. That’s why timing matters if you’re buying and selling before maturity. But if you hold them until they mature, you get every penny you’re owed, no matter what. That’s the quiet power of government-backed debt.

You’ll find these securities referenced in posts about fixed income, diversification, and retirement strategies. They’re not the flashiest part of investing, but they’re the foundation. Whether you’re just starting out or have been investing for years, you need to understand how they work. Below, you’ll find real guides that break down how to buy them, when to use them, and how they fit alongside other assets like dividend stocks, options, and emergency funds. No fluff. Just what you need to make smarter moves with your money.