Fintech for SMBs: Tools That Give Small Businesses Real Financial Power

When small business owners need cash fast, fintech for SMBs, technology that delivers financial services directly to small businesses through digital platforms. Also known as small business fintech, it cuts out the slow, paper-heavy process of traditional bank loans and puts control back in the owner’s hands. This isn’t theory—it’s what’s happening right now in QuickBooks, Xero, and other platforms used by millions of small businesses every day.

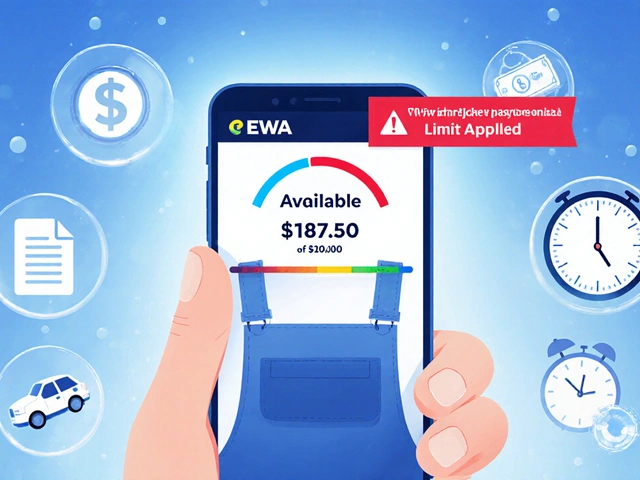

One of the biggest shifts is embedded lending, lending that happens inside the accounting software a business already uses. Instead of applying for a loan on a separate website, a shop owner can click a button in QuickBooks and get cash against unpaid invoices in under 24 hours. That’s invoice financing, turning money owed by customers into immediate working capital. No collateral, no 30-day wait. Just cash when you need it.

Behind the scenes, loan underwriting automation, using AI to review financial data and approve loans in minutes instead of weeks. is replacing the old system where a loan officer had to manually check bank statements and tax returns. Now, algorithms look at real-time sales data, payment history, and cash flow trends to decide if a business qualifies. That’s why more small businesses are getting approved today than ever before—even if they’ve been turned down by banks.

These tools don’t just give money. They give predictability. A restaurant owner can now plan for payroll because they know they can access funds when invoices are due. A contractor can take on a bigger job because they’re not stuck waiting 60 days for payment. This is fintech for SMBs not as a buzzword, but as a daily lifeline.

What you’ll find below are real, working examples of how these systems operate—their strengths, their limits, and how actual business owners use them to stay afloat and grow. No fluff. No marketing hype. Just the tools that are changing how small businesses survive and thrive in 2025.