Personal Savings Estimator

Based on research showing users who use open banking insights save 14% more, this calculator estimates your potential savings from better transaction categorization.

Your Potential Savings

Based on your spending patterns and open banking insights, you could save:

How this works: Your PFM app identifies unnecessary subscriptions and spending patterns. Research shows users who act on these insights save 14% more on average.

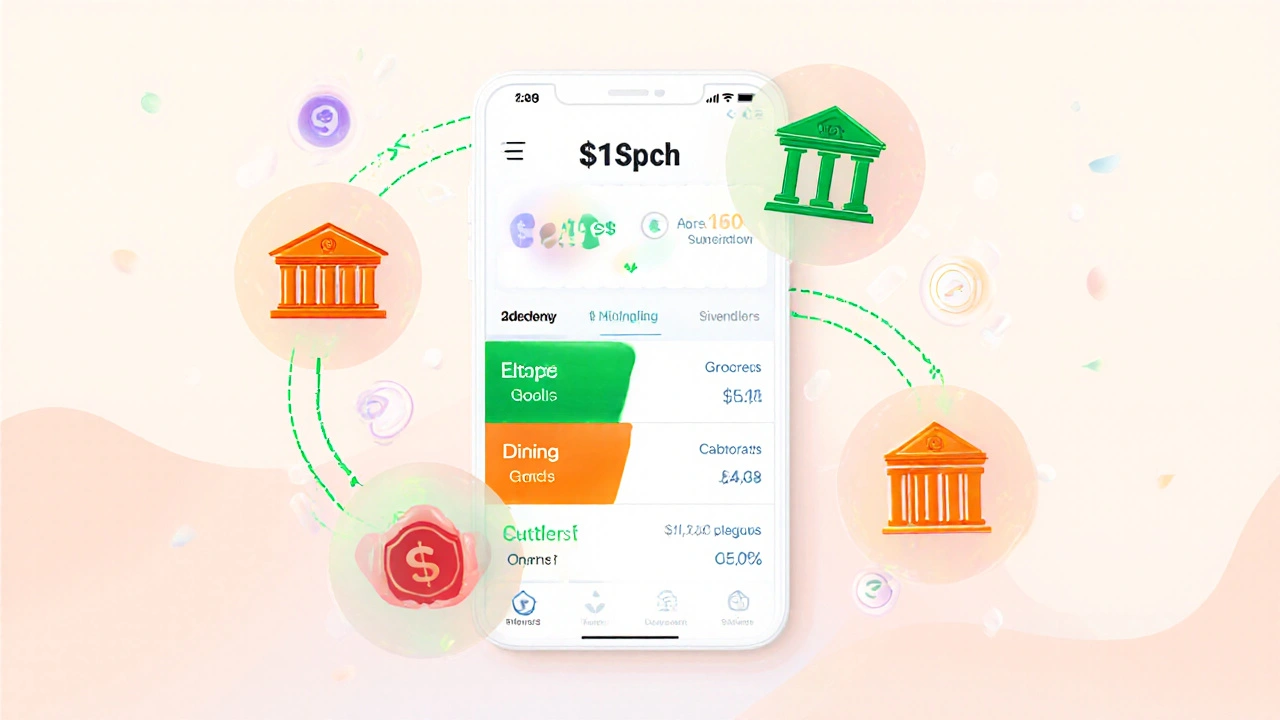

Imagine opening your phone and seeing exactly where your money went last month - not just as a list of transactions, but as clear categories: groceries, gas, streaming services, dining out. No manual logging. No spreadsheets. Just a clean breakdown that tells you why your savings goal is falling behind - and how to fix it. That’s not science fiction. It’s what open banking makes possible for Personal Financial Management (PFM) apps today.

What Open Banking Actually Does for PFM Apps

Open banking isn’t just about letting apps connect to your bank account. It’s about giving those apps access to real, structured, and secure transaction data through standardized APIs. Before open banking, PFM apps relied on users manually entering every purchase or uploading bank statements. That’s slow, error-prone, and most people quit after a week. Open banking changes that by pulling data directly from banks - automatically, securely, and in real time.The core of this system is transaction categorization. Every time you swipe your card at a grocery store, pay a utility bill, or order coffee, that transaction gets tagged. But it’s not just about labeling. The system reads the merchant name, location, amount, time, and even past behavior to decide if it’s "groceries," "dining," or "entertainment." Some systems go further - recognizing that a purchase from "Starbucks" might be a daily habit, while "Whole Foods" is a weekly bulk shop. That’s how you get insights, not just data.

How Categorization Turns Data Into Action

Categorization is the engine behind every useful feature in a modern PFM app. Without it, you just see a list of numbers. With it, you get context.- Spotting overspending: If your "dining out" category jumps 40% month-over-month, the app doesn’t just show you the total - it highlights the trend and compares it to your budget.

- Automated savings: If the app notices you spend $120 on coffee every month, it might suggest moving $30 to a savings goal labeled "Vacation Fund" - and even automate the transfer.

- Subscription tracking: It finds recurring charges you forgot about - like that $9.99 app you signed up for during a free trial last year.

- Peer comparisons: Some apps show you how your spending on "utilities" or "transportation" stacks up against others in your area, helping you see if you’re paying too much.

MX’s research on over 10 million users found that people who used these categorized insights saved 14% more and kept 15% higher deposit balances than those who didn’t. Why? Because knowing *why* you’re spending makes you change *how* you spend.

Why Manual Budgeting Still Fails

Most people try budgeting the old way: write down every expense, review it weekly, adjust. It sounds smart - until life happens. You forget to log a cash purchase. You’re tired after work. You miss a week. Suddenly, your budget is outdated before it’s even useful.Open banking removes that friction. You don’t need to remember to log anything. Your bank sends the data. The app sorts it. You get a weekly summary that’s accurate, timely, and actionable. Tink found that convenience in PFM apps directly translates to automation - and automation leads to consistent use. Users who get automatic categorization are 3x more likely to stick with the app long-term.

Security and Compliance: The Hidden Backbone

You might wonder: "Is it safe to let an app connect to my bank?" The answer is yes - if it follows open banking standards. In Europe, the Revised Payment Services Directive (PSD2) requires banks to offer secure API access. That means:- Only you can grant access - no one else can connect to your account without your permission.

- Authentication is two-factor - you’ll get a code on your phone or use biometrics to approve each connection.

- Data is encrypted in transit and at rest.

- Apps can’t store your login details - they only get access to transaction data, not your passwords.

This isn’t optional. Any PFM app that doesn’t follow these rules won’t work with major banks in the EU, UK, or anywhere with open banking laws. Even in the U.S., where regulation is looser, top providers like Plaid and MX follow the same security standards to earn user trust.

What Makes a PFM App Stand Out?

Not all PFM apps are created equal. Basic ones just show you spending totals. The best ones use categorization to deliver personalized insights.Here’s what separates the leaders:

- Merchant-level detail: Instead of just "shopping," it shows "Target," "Amazon," or "Lowe’s" - so you know if you’re overspending on one retailer.

- Pattern recognition: Notices that you always spend more on groceries before holidays, or that your energy bill spikes every January.

- Subscription alerts: Flags recurring payments you didn’t know you had - and lets you cancel them with one tap.

- Goal tracking: Links spending to goals: "You’re $800 away from your $3,000 emergency fund. At this rate, you’ll reach it in 4 months."

- Proactive nudges: "You’ve spent $200 on takeout this week - your average is $120. Want to try cooking tonight?"

GoCardless says the future of PFM is "fulfilling numerous needs" - and that means going beyond tracking to guiding. The apps that win are the ones that feel like a financial coach, not a calculator.

Real User Benefits: What People Actually Say

Users don’t care about APIs or compliance. They care about results.Here’s what real users report:

- "I finally paid off my credit card because I saw how much I was spending on Uber Eats every week. The app showed me exactly where the money was going - I couldn’t ignore it."

- "I didn’t realize I was paying $50 a month for two streaming services I never used. The app flagged them. I canceled both and saved $600 a year."

- "I set a goal to save $5,000 for a car. The app shows me progress every week. I’ve saved $3,200 in 8 months - and I didn’t even feel like I was cutting back."

AbbyBank found that users who get alerts for low balances or large purchases are 40% more likely to stay active in their app. Why? Because it feels personal. It’s not just data - it’s help.

The Bigger Picture: Where This Is All Heading

Open banking is evolving fast. The next wave isn’t just about bank accounts. It’s about connecting investment accounts, pensions, crypto wallets, and even utility bills into one dashboard.Mastercard predicts the next generation of PFM apps will use AI to predict your future cash flow - not just describe the past. Imagine an app that says: "Your rent is due in 5 days, but your paycheck won’t arrive until the 10th. Here’s what you can delay to avoid overdraft fees."

As more data becomes available, PFM apps will start offering tailored advice: "Based on your income and spending, you could qualify for a lower-interest loan. Here’s how." Or: "You’re on track to retire 5 years early if you keep saving at this rate."

The goal isn’t just to help people manage money - it’s to help them feel in control of their financial future.

Getting Started: What Developers Need to Know

If you’re building or choosing a PFM app, here’s what matters:- Choose a provider with strong categorization - not just account aggregation. Look for detailed merchant data, not just "miscellaneous."

- Make sure the provider supports Strong Customer Authentication (SCA) and complies with local regulations (PSD2 in Europe, CFPB guidelines in the U.S.).

- Test with real bank data. Different institutions format transactions differently. Your system needs to handle messy, inconsistent inputs.

- Offer alerts and goal tracking as core features - not add-ons. These are what keep users engaged.

- Don’t overpromise. Users don’t want a financial advisor. They want a tool that’s simple, accurate, and helps them make one smart decision this week.

The best PFM apps don’t try to do everything. They do one thing incredibly well: turn confusing transaction data into clear, actionable insight - and make users feel smarter about their money.

How does open banking improve transaction categorization in PFM apps?

Open banking gives PFM apps direct, secure access to real-time bank transaction data through standardized APIs. This eliminates manual entry and allows apps to use machine learning to automatically assign categories like "groceries," "utilities," or "entertainment" based on merchant names, transaction amounts, frequency, and historical patterns. The result is far more accurate and detailed categorization than users can achieve by logging expenses themselves.

Are open banking PFM apps safe to use?

Yes, when they follow open banking standards. In regions like the EU and UK, regulations like PSD2 require banks to offer secure API access with Strong Customer Authentication (SCA), meaning users must approve each connection using two-factor authentication (like a code sent to their phone). Apps cannot store your bank login details - they only receive transaction data under your permission. Data is encrypted both in transit and at rest, and providers undergo regular security audits.

What’s the difference between open banking PFM and traditional budgeting apps?

Traditional budgeting apps require users to manually enter transactions or upload bank statements, which leads to incomplete data and high abandonment rates. Open banking PFM apps connect directly to your bank accounts and automatically import every transaction in real time. This removes the effort barrier, making it far more likely users will stick with the app and actually use the insights it provides.

Can open banking PFM apps help me save money?

Yes - and research proves it. MX’s analysis of over 10 million users found that people who regularly used PFM features with open banking data saw a 14% increase in savings balances and 15% higher deposit balances compared to those who didn’t. This happens because users gain clarity on spending patterns, get alerts for unnecessary subscriptions, and receive personalized suggestions to cut back - turning awareness into action.

What should I look for in a PFM app powered by open banking?

Look for apps that offer detailed categorization (not just "miscellaneous"), subscription alerts, goal tracking with progress updates, and proactive insights like "You’re spending 40% more on dining out this month." Avoid apps that only show transaction totals. The best ones turn data into advice - helping you make smarter decisions without requiring you to be a finance expert.

Kenny McMiller

November 14, 2025 AT 19:59Open banking’s real magic isn’t the API-it’s the ontological shift in how we conceptualize financial behavior. Transaction data, when normalized through ML-driven categorization, becomes a semiotic field where spending patterns encode latent desires, cognitive biases, and temporal discounting tendencies. We’re not just tracking expenses-we’re reverse-engineering identity through merchant metadata. That $120/month coffee habit? It’s not about caffeine. It’s about autonomy, ritual, and the illusion of control in an algorithmically mediated life.

And yeah, the 14% savings bump? That’s not behavioral economics-it’s epistemic humility. When the system mirrors your chaos back at you with clean taxonomy, you can’t rationalize anymore. You’re forced to confront the dissonance between who you think you are and what your bank statement says you value.

Most PFM apps treat this like a dashboard. It’s not. It’s a mirror. And mirrors hurt.

PS: If your app labels ‘Starbucks’ as ‘entertainment’ and ‘Whole Foods’ as ‘groceries’ without context, you’re not using AI-you’re using a thesaurus with a Wi-Fi connection.

Dave McPherson

November 14, 2025 AT 20:07Ugh. Another ‘open banking will save your soul’ thinkpiece. Newsflash: most people don’t care about ‘categorization’-they care about not getting charged $4.99 for a ‘premium’ app they deleted in 2021. I’ve seen these apps. They flag ‘Amazon’ as ‘shopping’ and then wonder why I’m ‘overspending’ on ‘miscellaneous.’

Meanwhile, my bank’s app just says ‘$87.32 at Target’ and I’m like, ‘yep, bought socks.’ No algorithm needs to interpret my life. The data’s right there. Stop overengineering human behavior with buzzwords.

Also, ‘proactive nudges’? That’s just surveillance with a smiley face. I don’t need an app telling me to cook. I need fewer subscription traps and more transparency from banks-not some Silicon Valley guru pretending to be my financial therapist.

Julia Czinna

November 15, 2025 AT 08:00Dave, you’re not wrong. A lot of these apps do overcomplicate things. But I’ve used one that actually got it right-it noticed I was paying $15/month for a meditation app I never opened, canceled it for me with one tap, and then quietly moved $15 to my vacation fund without asking. No nagging. No jargon. Just… helpful.

It didn’t try to ‘reverse-engineer my identity.’ It just noticed a pattern I ignored. That’s the difference between a tool and a sales pitch.

Also, I used to hate budgeting. Now I check my balance once a week and feel calm. That’s not magic. That’s good UX. And yeah, it’s because of open banking-not because it’s fancy, but because it’s silent and reliable.

Also, thank you for calling out the ‘financial therapist’ nonsense. We don’t need more advice. We need fewer invisible charges.

🙂

RAHUL KUSHWAHA

November 16, 2025 AT 14:48From India, we don’t have open banking yet… but I read this and feel hopeful. Many here still use cash or handwritten ledgers. If this kind of quiet, smart help could reach people without loud ads or pressure… it could change lives. Small steps. No rush. Just clarity.

Thank you for writing this. 🙏