Taxable Brokerage Account: How to Use It to Keep More of Your Investment Gains

When you open a taxable brokerage account, a standard investment account where you buy and sell stocks, ETFs, and bonds, and pay taxes on gains and income each year. Also known as a non-retirement brokerage account, it’s the most flexible tool you have for investing—no contribution limits, no required withdrawals, and you can pull money out anytime. But that freedom comes with a cost: every dividend, interest payment, and capital gain gets taxed in the year it happens. Most people treat it like a savings account with stocks, but that’s where they lose money. The real power of a taxable brokerage account isn’t just what you buy—it’s what you don’t buy there.

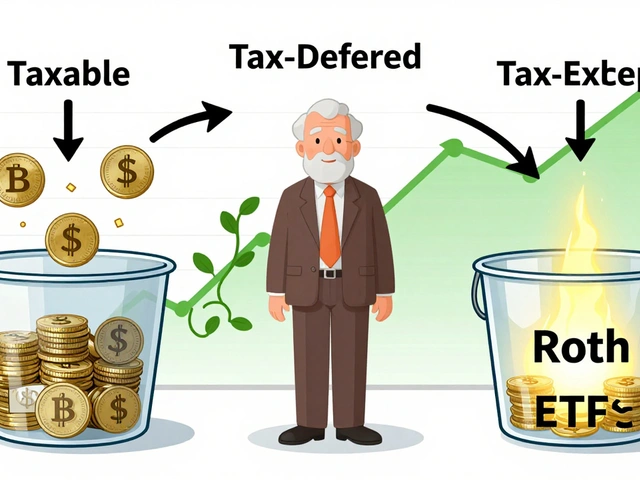

That’s where tax coordination, the strategy of placing different types of investments in the right accounts to minimize taxes comes in. Think of your money like pieces in a puzzle. High-growth stocks and ETFs? Save them for your Roth IRA or taxable account. Bonds and dividend stocks that throw off yearly income? Those belong in your 401(k) or other tax-deferred accounts, accounts where you don’t pay taxes until you withdraw, like traditional IRAs or 401(k)s. Why? Because bonds generate income every year, and that income gets taxed at your regular rate in a taxable account. In a tax-deferred account, it grows untouched until withdrawal. Meanwhile, stocks held long-term in a taxable account get taxed at the lower capital gains rate—sometimes as low as 0%.

And it’s not just about what you own. How you rebalance matters too. If you sell a stock that’s doubled in your taxable account to buy another, you trigger a capital gains tax. But if you do the same trade inside your 401(k), no tax hits. That’s why smart investors use their taxable account for long-term holds and let their tax-deferred accounts handle the trading. It’s a small tweak that can add up to 0.75% extra returns every year—without taking on more risk.

Some people avoid taxable accounts because they hear "taxes" and think it’s a trap. But it’s not. It’s a tool. Used right, it gives you control over when and how you pay taxes. You can harvest losses to offset gains, time big sales for lower-income years, and even pass assets to heirs with a step-up in basis. This isn’t Wall Street jargon—it’s everyday math that works for anyone who invests.

Below, you’ll find real guides on how to use your taxable brokerage account with other accounts to cut taxes, how to rebalance without getting hit with a big bill, and how to pick the right broker so fees don’t eat your gains. No fluff. No theory. Just what works.